What is a recession?

A recession is a significant, widespread, and prolonged downturn in economic activity. A common rule of thumb is that two consecutive quarters of negative gross domestic product (GDP) growth mean recession, although more complex formulas are also used.

Economists at the National Bureau of Economic Research (NBER) measure recessions by looking at nonfarm payrolls, industrial production, and retail sales, among other indicators, going far beyond the simpler (although not as accurate) two-quarters of negative GDP measure.

However, the NBER also says there is “no fixed rule about what measures contribute information to the process or how they are weighted in our decisions.”

A downturn must be deep, pervasive, and lasting to qualify as a recession by the NBER’s definition, but these calls come after the fact: It is not a clear formula to identify a recession as soon as one begins.

Understanding Recessions

Since the Industrial Revolution, most economies have grown steadily and economic contractions are an exception, although recessions are still common. Between 1960 and 2007, there were 122 recessions that affected 21 advanced economies roughly 10% of the time, according to the International Monetary Fund (IMF).

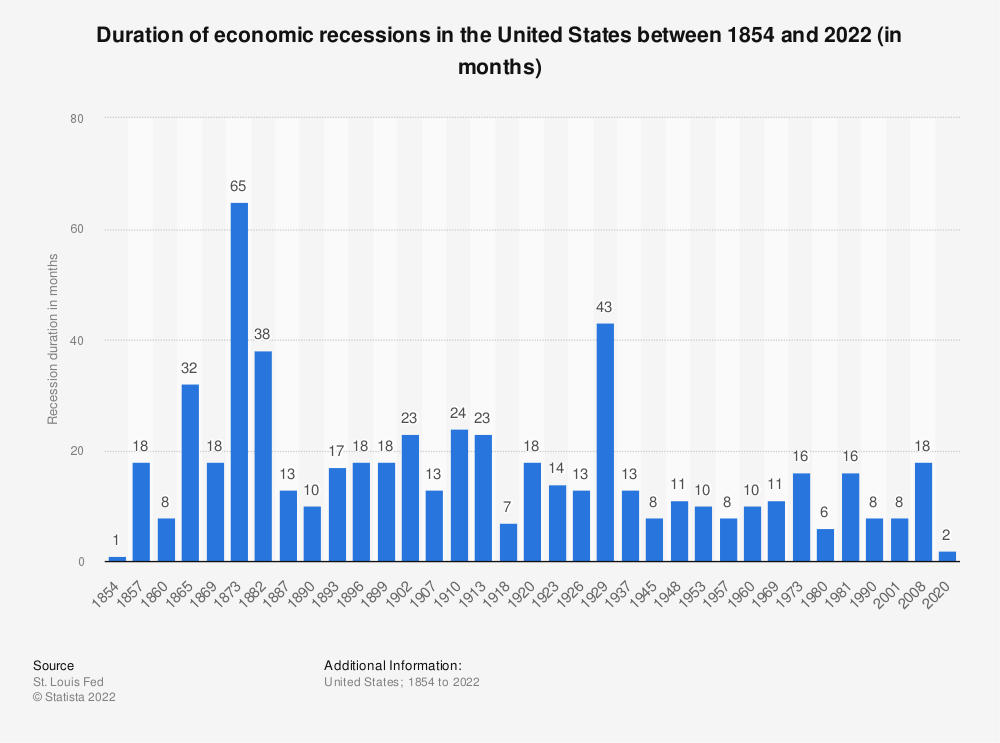

Economic Expansions by Duration

Economic expansions begin at the trough of a business cycle – its lowest point – and end at its peak, after which the economy begins to contract, kicking off an economic recession.

Recessions are usually clearly identified only after they are over. Investors, economists, and employees may also have very different experiences in terms of when a recession is at its worst.

Equities markets often decline before an economic downturn, so investors may assume a recession has begun as investment losses accumulate and corporate earnings decline, even if other measures of recession remain healthy, such as consumer spending and unemployment.

Conversely, since unemployment often remains high long after the economy hits bottom, workers may perceive a recession as continuing for months or even years after economic activity recovers.

What Predicts a Recession?

While there is no single, sure-fire predictor of recession, an inverted yield curvehas come before each of the 10 U.S. recessions since 1955, although not every period of inverted yield curve was followed by recession.

When the yield curve is normal, short term yields are lower than long term yields. This is because longer-term debt has more duration risk. For example, a 10-year bond usually yields more than a 2-year bond as the investor is taking a risk that future inflation or higher interest rates could lower the bond’s value before it can be redeemed. So, in this case the yield goes up over time, creating an upward yield curve.

The yield curve inverts if yields on longer-dated bonds go down while yields on shorter term bonds go up. The rise of near term interest rates can tip the economy into a recession. The reason why the yield on long term bonds drops below that on short term bonds is because traders anticipate near term economic weakness leading to eventual interest rate cuts.

Investors also look at a variety of leading indicators to predict recession. These include the ISM Purchasing Managers Index, the Conference Board Leading Economic Index, and the OECD Composite Leading Indicator.

What Causes Recessions?

Numerous economic theories attempt to explain why and how an economy goes into recession. These theories can be broadly categorized as economic, financial, psychological, or a combination of these factors.

Some economists focus on economic changes, including structural shifts in industries, as most important. For example, a sharp, sustained surge in oil prices can raise costs across the economy, leading to recession.

Some theories say financial factors cause recessions. These theories focus on credit growth and the accumulation of financial risks during good economic times, the contraction of credit and money supply when recession starts, or both. Monetarism, which says recessions are caused by insufficient growth in money supply, is a good example of this type of theory.

Other theories focus on psychological factors, such as over-exuberance during economic booms and deep pessimism during downturns to explain why recessions occur and persist. Keynesian economics focuses on the psychological and economic factors that can reinforce and prolong recessions. The concept of a Minsky Moment, named for economist Hyman Minsky, combines the two to explain how bull-market euphoria can encourage unsustainable speculation.